[ad_1]

There is 1 crucial retirement finance concern that is so difficult that most investors get it incorrect even when you convey to them the respond to in advance.

The query focuses on “life expectancy,” and useless to say answering it the right way is an vital prerequisite to excellent retirement organizing. Underestimate how extensive you are probable to live and you operate the danger of outliving your funds. If you overestimate it, in contrast, you run a great likelihood of leaving a whole lot of revenue on the table, so to speak—money that you could or else spend to love your retirement.

Scientists have known for some time that most of us have a bad knowledge of everyday living expectancy. At the beginning of this 12 months, for instance, the TIAA Institute and George Washington University’s World-wide Economical Literacy Excellence Heart (GFLEC) produced outcomes of a study exhibiting that two-thirds of U.S. grownups had been unable to reply standard queries these as “what is lifestyle expectancy among the 60-12 months-aged adult men in the U.S.” (I devoted a mid-January column to this study.)

That is disheartening ample, since you just cannot approach for a retirement if you never know how prolonged it will final. But even far more depressing are the benefits of comply with up research that the TIAA Institute/GFLEC released two months ago. The researchers observed that “longevity literacy” doesn’t strengthen even when you give absent the remedy.

To enjoy what the scientists found out, see if you can appropriately remedy the following problem that they posed to the grownups getting their study: “If lifetime expectancy among 65-calendar year-old folks is 20 many years, which of the subsequent statements is real?”

- About just one-half of 65-yr-olds will reside previous age 85

- The huge bulk of 65-year-olds will not are living previous age 85

- About a single-fifty percent of 65-12 months-olds will die amongst age 84 and 86

The proper remedy is the first. That’s simply because, as the scientists write, the specific indicating of life expectancy “is the quantity of supplemental many years beyond which 1-half of the team members will are living, even though the other just one-50 % will not.”

Never be way too hard on by yourself if you acquired this mistaken only 35% of survey respondents received it right.

The most widespread response between respondents who got it mistaken was the next one, and you can fully grasp why. Upon currently being told that our lifestyle expectancy is, say, 85 many years, most of us think that the prudent issue to do is determine out how to shell out for a retirement that lasts until eventually then. In simple fact, even so, half of us can assume to stay more time than that, which in convert means 50% of us are possible to outlive our funds if we build a retirement economic system that lasts only via our everyday living expectancy.

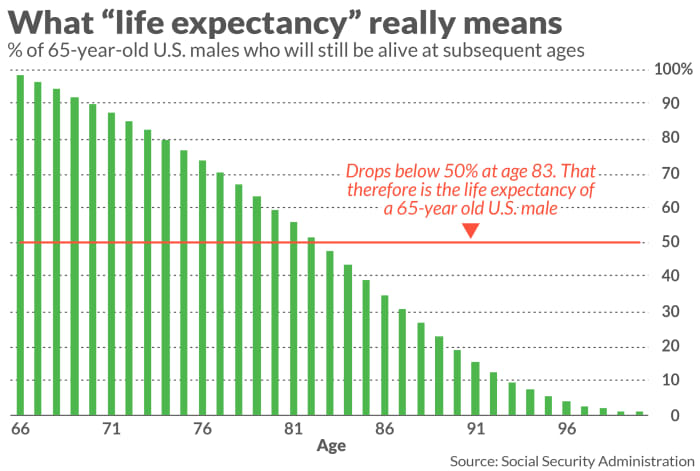

This real meaning of “life expectancy” is illustrated in the accompanying chart. It plots the share of 65-12 months-outdated U.S. males who are nevertheless alive at various subsequent ages. Observe that 50% will nonetheless be alive at age 83, according to the most recent Social Stability actuarial tables, which is why Social Stability studies the lifetime expectancy of a 65-calendar year-outdated male to be 83. (A chart for 65-yr-outdated ladies would extend out more the share of them still alive does not drop below 50% right until age 86.)

What if you want only a 10% likelihood of outliving your income? Then 65-year-old males will need to figure out how to pay back for retirement via age 93. If you want only a 5% chance, you want to finance your retirement standard of residing via age 96. (For gals it is 96 and 98, respectively.)

Supplied this new being familiar with of daily life expectancy, many of you may now want to reconstruct your retirement fiscal plans. But it is much better to know this now than later on. Forewarned is forearmed.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment decision newsletters that pay back a flat fee to be audited. He can be arrived at at [email protected].

[ad_2]

Source hyperlink